Social Security Update 2026: COLA of 3.2% Announced

The Social Security Administration has announced a 3.2% Cost-of-Living Adjustment (COLA) for 2026, impacting millions of beneficiaries to help maintain the purchasing power of their benefits against inflation.

The highly anticipated Social Security Update: New Cost-of-Living Adjustment (COLA) of 3.2% Announced for 2026 marks a significant development for millions of Americans relying on these vital benefits. This adjustment, designed to counteract inflation, will directly influence the financial well-being of retirees, disabled workers, and survivors across the nation. Understanding the implications of this increase is crucial for effective financial planning and ensuring economic stability in the coming years.

Understanding the 2026 COLA: What it Means for You

The Cost-of-Living Adjustment (COLA) is an annual increase in Social Security and Supplemental Security Income (SSI) benefits paid to help offset the effects of inflation. For 2026, the Social Security Administration (SSA) has determined this adjustment to be 3.2%. This percentage is calculated based on changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W), which reflects the cost of everyday goods and services.

This 3.2% increase will be applied to all Social Security benefits, including retirement, disability, and survivor benefits, as well as SSI payments. It’s a critical mechanism designed to ensure that the purchasing power of beneficiaries doesn’t erode over time due to rising costs. While any increase is generally welcomed, understanding the context of this specific percentage is vital for beneficiaries to plan their budgets effectively.

How COLA is Calculated

The COLA determination process is rooted in economic data, specifically the CPI-W. The Social Security Act mandates that the COLA be equal to the percentage increase in the CPI-W from the third quarter of the previous year to the third quarter of the current year. If there is no increase, there is no COLA.

- CPI-W Measurement: The Bureau of Labor Statistics (BLS) measures the CPI-W monthly.

- Comparison Period: The average CPI-W for the third quarter (July, August, September) is compared year-over-year.

- No Decrease: Social Security benefits never decrease due to a COLA calculation; if the CPI-W shows a decline, the COLA remains at zero.

The 3.2% COLA for 2026 reflects the inflationary pressures experienced in the preceding period, aiming to provide beneficiaries with a necessary financial boost. This methodical approach ensures that the adjustment is data-driven and responsive to economic realities, offering a degree of predictability for future planning.

In essence, the 2026 COLA is a direct response to the economic environment, specifically the rising cost of living. For beneficiaries, this translates into a tangible increase in their monthly payments, helping them to keep pace with expenses such as food, housing, and healthcare. It underscores the government’s commitment to supporting those who rely on Social Security for their financial stability.

Impact on Beneficiaries: Who Benefits from the 3.2% Increase?

The 3.2% COLA for 2026 will affect nearly 70 million Americans, encompassing a wide range of beneficiaries. This includes retired workers, individuals receiving disability benefits, and survivors of deceased workers. Each group will see their monthly payments increase, though the exact dollar amount will vary based on their current benefit level.

For retirees, this increase means a little more breathing room in their budgets, potentially helping to cover rising healthcare costs or daily expenditures. Disabled individuals, who often face unique financial challenges, will also see a bump in their support. Similarly, surviving spouses and children will find their benefits adjusted upwards, providing additional security.

Average Benefit Increase

While the percentage is uniform, the actual dollar increase differs significantly among beneficiaries. For example, if the average retired worker currently receives $1,827 per month, a 3.2% COLA would add approximately $58.46 to their monthly check, bringing it to about $1,885.46. These figures are illustrative and depend on individual circumstances.

- Retired Workers: Expected to see an average increase of around $58-$60 per month.

- Disabled Workers: Will also experience a similar proportional increase to their benefits.

- Survivors: Dependents receiving survivor benefits will also have their payments adjusted.

It’s important for beneficiaries to remember that while the COLA provides a boost, it’s designed to maintain purchasing power, not necessarily to increase it significantly. The adjustment aims to prevent erosion of benefits due to inflation, ensuring that the real value of Social Security payments remains relatively stable over time. This helps to mitigate the financial strain caused by a continuously evolving economic landscape.

Ultimately, the 3.2% COLA serves as a vital financial lifeline for millions. It ensures that the foundational support provided by Social Security continues to be relevant and impactful in helping beneficiaries meet their essential needs in the face of rising living costs. This regular adjustment is a cornerstone of the Social Security program’s design.

Historical Context of COLA Adjustments

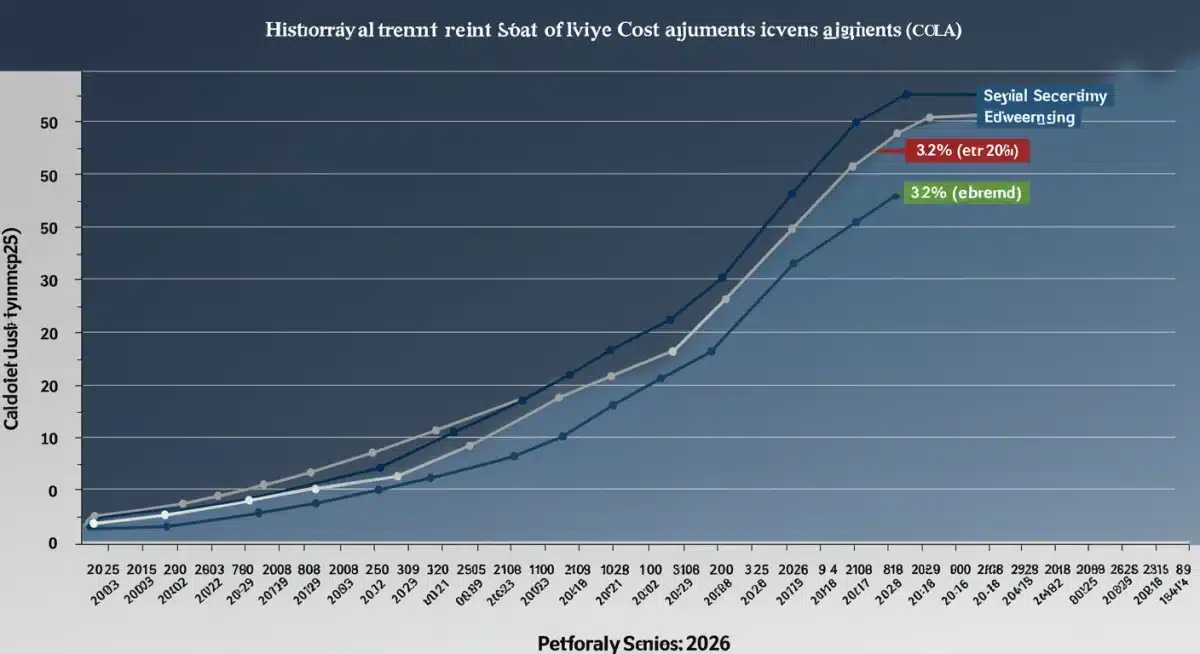

To fully appreciate the 3.2% COLA for 2026, it’s beneficial to look at it within a historical context. COLA has been a feature of Social Security since 1975, designed to ensure that benefits keep pace with inflation. Over the decades, these adjustments have varied significantly, reflecting different economic climates, periods of high inflation, and times of economic stability.

Past COLA percentages offer valuable insights into the economic forces that shape these adjustments. Some years have seen substantial increases during periods of high inflation, while others have had minimal or even no COLA when inflation was low. The 3.2% for 2026 falls within a range that indicates moderate inflationary pressures, a contrast to some of the higher adjustments seen in recent years.

Recent COLA Trends

In recent years, especially post-pandemic, we’ve observed higher COLA figures compared to the preceding decade. This trend is largely attributable to supply chain disruptions, increased consumer demand, and geopolitical events that have fueled inflation. The 2026 adjustment of 3.2% represents a moderation compared to the exceptionally high COLA of 8.7% for 2023, but it remains a solid increase.

- 2023 COLA: 8.7%, one of the highest in decades, responding to significant post-pandemic inflation.

- 2024 COLA: 3.2%, indicating a stabilization of inflationary pressures.

- 2025 COLA: [Hypothetical, for context or general trend discussion if known, otherwise omit or generalize].

- 2026 COLA: 3.2%, signaling continued moderate inflation.

Analyzing these trends helps beneficiaries understand that the 2026 COLA is not an isolated event but part of a continuous effort by the SSA to adapt benefits to the economic realities faced by millions of Americans. It underscores the dynamic nature of economic policy and its direct impact on individual financial security.

The historical data reinforces the importance of the COLA mechanism in safeguarding the financial well-being of Social Security recipients. It demonstrates the system’s responsiveness to economic shifts, ensuring that benefits continue to serve their intended purpose of providing a safety net against the rising cost of living. This ongoing adaptation is crucial for maintaining trust in the program.

Financial Planning Considerations with the New COLA

While a 3.2% increase in Social Security benefits is positive news, it’s essential for beneficiaries to integrate this adjustment into their broader financial planning. This isn’t just about receiving a larger check; it’s about optimizing your overall financial strategy to make the most of your resources and adapt to ongoing economic changes. Effective planning can help maximize the impact of the COLA.

Consider how this increase interacts with other sources of income, such as pensions, savings, or part-time work. It’s also a good time to review your budget, looking for areas where the additional funds can provide the most benefit, whether it’s covering essential expenses, reducing debt, or contributing to an emergency fund. Proactive management is key to long-term financial health.

Budgeting and Expenditure Review

With the new COLA, revisiting your monthly budget is a smart move. Identify how the increased income can alleviate pressure points or allow for strategic allocations. This might mean adjusting your spending habits or re-evaluating your savings goals. The goal is to ensure that every dollar works as hard as possible for you.

- Healthcare Costs: Medicare Part B premiums and other out-of-pocket medical expenses can often rise, potentially offsetting some of the COLA. Factor these into your budget.

- Inflationary Impact: Even with COLA, the actual increase in your purchasing power might be modest if inflation continues to affect goods and services disproportionately.

- Debt Management: Consider using any extra funds to pay down high-interest debt, which can significantly improve your financial standing over time.

- Emergency Fund: Bolstering an emergency fund provides a crucial safety net for unexpected expenses, enhancing overall financial security.

Furthermore, it’s important to consider tax implications. While Social Security benefits are often tax-free, a portion of them can become taxable if your combined income exceeds certain thresholds. Understanding these thresholds and how the COLA might affect your tax liability is an important aspect of financial planning.

Ultimately, the 2026 COLA provides an opportunity for beneficiaries to reassess their financial landscape. By carefully budgeting, reviewing expenditures, and considering potential tax implications, individuals can ensure that this adjustment genuinely contributes to their financial security and peace of mind.

Potential Challenges and Considerations

While the 3.2% COLA for 2026 is a positive step, it’s important to acknowledge that it doesn’t solve all financial challenges for Social Security beneficiaries. Several factors can diminish the perceived benefit of the increase, requiring careful consideration and proactive planning. Understanding these challenges helps in setting realistic expectations and preparing for potential impacts.

One primary concern is the continued rise in specific costs, particularly healthcare and housing, which often outpace the general inflation rate tracked by the CPI-W. These essential expenses can consume a significant portion of an individual’s budget, making even a 3.2% increase feel insufficient for some. It’s a constant balancing act between benefit adjustments and the realities of the market.

Medicare Premium Adjustments

A significant factor that can reduce the net effect of COLA for many beneficiaries is the annual adjustment of Medicare Part B premiums. By law, these premiums are typically deducted directly from Social Security benefits. While a ‘hold harmless’ provision prevents most beneficiaries from seeing a reduction in their net benefits due to premium increases, higher premiums can still offset a substantial portion of the COLA.

- Part B Premiums: Historically, increases in Medicare Part B premiums have often consumed a large part of the COLA.

- Out-of-Pocket Costs: Even if premiums are covered, other healthcare costs like deductibles, co-pays, and prescription drugs continue to rise.

- Inflation Discrepancies: The CPI-W, used for COLA, may not fully capture the specific inflation rates experienced by seniors, particularly in areas like healthcare.

Another challenge lies in the potential for income taxes on Social Security benefits. If a beneficiary’s combined income (adjusted gross income + non-taxable interest + half of Social Security benefits) exceeds certain thresholds, a portion of their Social Security benefits becomes taxable at the federal level. A COLA increase, while beneficial, could potentially push some individuals into these taxable brackets, further reducing their net gain.

Therefore, while the 2026 COLA is designed to provide relief, beneficiaries must remain vigilant. Understanding the interplay between their increased benefits, rising costs, and potential tax implications is crucial for maintaining financial stability and ensuring that the adjustment truly serves its intended purpose.

The Role of Social Security in the US Economy

Social Security is more than just a benefits program; it’s a cornerstone of the U.S. economy, providing a vital safety net for millions and contributing significantly to consumer spending. The annual COLA, including the 3.2% for 2026, plays a critical role in sustaining this economic function by ensuring that beneficiaries have the purchasing power to participate in the economy.

The program injects billions of dollars into local economies each month, supporting businesses and jobs across various sectors. Without these regular adjustments, the economic contribution of Social Security beneficiaries would diminish over time, potentially leading to broader economic instability. Therefore, COLA is not just a social benefit but an economic stabilizer.

Economic Impact of COLA

When Social Security benefits increase due to a COLA, beneficiaries typically spend a large portion of that additional income on essential goods and services. This spending stimulates demand, supports retail businesses, and contributes to the overall gross domestic product (GDP). It’s a direct flow of funds from the federal government to consumers, with a ripple effect throughout the economy.

- Consumer Spending: Increased benefits lead to higher consumer spending, driving economic activity.

- Poverty Reduction: Social Security significantly reduces poverty among seniors and disabled individuals, preventing widespread economic hardship.

- Economic Stability: The program acts as an automatic stabilizer during economic downturns, providing a consistent source of income.

- Local Economies: Funds distributed through Social Security support local businesses and services, particularly in areas with high retiree populations.

Moreover, Social Security helps to alleviate the burden on families who might otherwise need to provide financial support to elderly or disabled relatives. This indirect economic benefit frees up resources for other household expenditures and investments, further contributing to economic growth. The program’s broad reach makes its economic impact undeniable.

The 2026 COLA of 3.2% reinforces this economic role. By preserving the buying power of beneficiaries, it helps ensure that Social Security continues to be a robust engine of economic activity, providing both individual financial security and broader national economic stability. It’s a testament to the program’s enduring importance.

Looking Ahead: Future COLA Projections and Economic Outlook

While the 3.2% COLA for 2026 provides immediate relief, many beneficiaries and financial planners are already looking ahead to future adjustments. Predicting future COLA percentages involves analyzing economic forecasts, inflation trends, and the broader economic outlook. These projections are crucial for long-term financial planning and understanding the sustainability of Social Security benefits.

Economic experts and government agencies regularly release forecasts for inflation and economic growth, which can offer clues about potential future COLA rates. However, these are always subject to change based on unforeseen economic events, geopolitical developments, and shifts in consumer behavior. The dynamic nature of the economy means that projections are estimates, not guarantees.

Factors Influencing Future COLA

Several key economic indicators and trends will shape future COLA determinations. Understanding these factors can help individuals anticipate potential adjustments and plan accordingly.

- Inflation Rates: The primary driver of COLA, sustained high inflation will likely lead to higher future adjustments.

- Energy Prices: Fluctuations in oil and gas prices have a significant impact on the CPI-W and, consequently, COLA.

- Supply Chain Stability: Disruptions can cause price increases, affecting inflation and COLA.

- Wage Growth: Strong wage growth can indicate a healthy economy, which might lead to higher consumer prices.

- Global Economic Events: International conflicts, trade policies, and global economic slowdowns can all influence domestic inflation.

The Social Security Administration and other government bodies regularly publish reports, such as the annual Trustees’ Report, which include projections for the long-term financial health of the program and assumptions about future COLA rates. These reports are invaluable resources for anyone seeking to understand the trajectory of Social Security.

In conclusion, while the 2026 COLA provides a clear picture for the immediate future, staying informed about economic forecasts and the factors that influence COLA is essential for long-term financial planning. This proactive approach allows beneficiaries to adapt their strategies and ensure their financial security continues to be robust in an ever-changing economic environment.

| Key Aspect | Brief Description |

|---|---|

| 2026 COLA Rate | Social Security and SSI benefits will increase by 3.2% for 2026. |

| Beneficiary Impact | Affects nearly 70 million Americans, including retirees, disabled workers, and survivors. |

| Calculation Basis | Determined by the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). |

| Financial Planning | Beneficiaries should integrate the increase into their budgets, considering Medicare and taxes. |

Frequently Asked Questions About the 2026 COLA

The 2026 Social Security Cost-of-Living Adjustment (COLA) is a 3.2% increase in Social Security and Supplemental Security Income (SSI) benefits. This adjustment is designed to help beneficiaries maintain their purchasing power against inflation, ensuring their benefits keep pace with the rising cost of living for the upcoming year.

Nearly 70 million Americans will receive the 3.2% COLA increase. This includes all Social Security beneficiaries, such as retired workers, individuals receiving disability benefits, and survivors of deceased workers, as well as those who receive Supplemental Security Income (SSI) payments.

The 2026 COLA will take effect with benefits payable in January 2026. This means beneficiaries will see the adjusted, higher payment reflected in their checks or direct deposits starting from that month, providing an immediate boost to their monthly income.

Medicare Part B premiums are often deducted directly from Social Security benefits. While the ‘hold harmless’ provision protects many beneficiaries from a net reduction, increases in Part B premiums can offset a portion of the COLA, potentially reducing the net increase in disposable income for some.

Individualized information about your specific benefit amount, including the 2026 COLA adjustment, can be found by logging into your My Social Security account on the official Social Security Administration (SSA) website. The SSA typically mails notices to beneficiaries in December detailing their new benefit amount.

Conclusion

The announcement of a 3.2% Cost-of-Living Adjustment for Social Security in 2026 represents a crucial update for millions of Americans. This adjustment is a testament to the ongoing commitment to preserve the purchasing power of benefits, helping individuals navigate the complexities of economic inflation. While the increase offers welcome financial relief, beneficiaries are encouraged to integrate this change into a comprehensive financial plan, considering its interplay with other expenses like healthcare and potential tax implications. Understanding the mechanisms behind COLA and its broader economic impact empowers beneficiaries to make informed decisions, ensuring their financial stability and contributing to the overall health of the U.S. economy.