Medicare Part D Changes 2026: Drug Benefits & Cost Savings

The significant Medicare Part D changes for 2026 aim to reduce out-of-pocket prescription drug costs for beneficiaries, introducing a new $2,000 cap and altering how plans cover medication expenses, ultimately enhancing affordability and access.

Understanding Prescription Drug Benefits in 2026: A Deep Dive into Medicare Part D Changes and Cost Savings is crucial for millions of Americans. As we approach 2026, significant adjustments to Medicare Part D are on the horizon, promising both challenges and opportunities for beneficiaries. These impending changes are designed to reshape how prescription drug costs are managed, aiming to provide greater financial relief and improved access to necessary medications. By staying informed about these updates, individuals can better navigate their healthcare decisions and optimize their drug coverage.

The Evolution of Medicare Part D: A Historical Context

Medicare Part D, established in 2006, was designed to help Medicare beneficiaries cover the costs of prescription drugs. Before its inception, many seniors faced exorbitant out-of-pocket expenses for their medications, leading to difficult choices between essential drugs and other living costs. The introduction of Part D marked a pivotal moment, providing a framework for private insurance companies to offer prescription drug plans, often alongside Medicare Advantage plans.

Over the years, Part D has undergone several modifications, primarily to address rising drug costs and improve beneficiary protections. Early iterations included the infamous ‘donut hole’ or coverage gap, a period where beneficiaries paid a higher percentage of their drug costs. While this gap has been progressively narrowed, the journey toward more affordable prescription drugs has been continuous. Each legislative change has aimed to refine the program, balancing affordability for beneficiaries with the sustainability of the healthcare system.

Key Milestones in Part D History

- 2006 Program Launch: Medicare Part D officially begins, offering prescription drug coverage through private plans.

- Affordable Care Act (ACA) 2010: The ACA introduced provisions to gradually close the coverage gap, reducing the beneficiary’s share of costs in the donut hole.

- Bipartisan Budget Act of 2018: Further accelerated the closure of the coverage gap for brand-name drugs.

- Inflation Reduction Act (IRA) 2022: This landmark legislation laid the groundwork for the most significant changes, including drug price negotiation and the upcoming 2026 reforms to Part D.

These historical developments illustrate a consistent effort to enhance the program’s value for beneficiaries. The changes slated for 2026 are a direct continuation of this trend, representing a substantial step forward in reducing the financial burden of prescription medications. Understanding this historical context helps to appreciate the magnitude and intention behind the upcoming reforms.

In conclusion, Medicare Part D’s evolution reflects a dynamic response to the nation’s prescription drug challenges. From its initial rollout to the present day, legislative actions have aimed to make drug coverage more comprehensive and affordable. The 2026 changes are not isolated events but rather part of a larger narrative of continuous improvement and adaptation within the Medicare system.

Understanding the Inflation Reduction Act’s Impact on Part D in 2026

The Inflation Reduction Act (IRA) of 2022 is a game-changer for Medicare Part D, with its full impact beginning to materialize in 2026. This legislation introduces several groundbreaking provisions designed to lower prescription drug costs for seniors and people with disabilities. A cornerstone of these reforms is the establishment of a $2,000 annual out-of-pocket cap for Part D beneficiaries, a development that will significantly alter the landscape of drug expenses.

Prior to the IRA, there was no hard cap on out-of-pocket spending in Part D, leaving some beneficiaries exposed to unlimited costs, especially those with high-cost specialty drugs. The $2,000 cap is a monumental shift, providing predictable financial protection. This means that once a beneficiary spends $2,000 out of their own pocket on covered prescription drugs in a year, they will not have to pay any more for the remainder of that year, regardless of the total cost of their medications.

Key IRA Provisions Affecting Part D in 2026

- $2,000 Out-of-Pocket Cap: The most impactful change, limiting annual out-of-pocket costs for covered Part D drugs.

- Elimination of the 5% Coinsurance: After reaching the catastrophic phase, beneficiaries currently pay 5% coinsurance. The IRA eliminates this, meaning no out-of-pocket costs beyond the $2,000 cap.

- Manufacturer Discounts: Drug manufacturers will be responsible for a greater share of costs in the catastrophic phase, reducing the burden on beneficiaries and Medicare.

- Insurer Responsibilities: Part D plans will also bear a larger share of drug costs in the catastrophic phase, further aligning incentives to manage costs.

These changes are projected to offer substantial relief to beneficiaries, particularly those with chronic conditions requiring expensive medications. The predictability of the $2,000 cap allows for better financial planning and reduces the risk of unexpected medical debt. It also encourages adherence to prescribed treatments, as the fear of spiraling costs is mitigated.

In essence, the IRA’s provisions for 2026 are poised to make prescription drugs more accessible and affordable for millions. By capping out-of-pocket spending and redistributing cost responsibilities among manufacturers, plans, and the government, the law aims to create a more equitable and sustainable Part D program. Beneficiaries should begin preparing now to understand how these changes will impact their specific drug costs and plan choices.

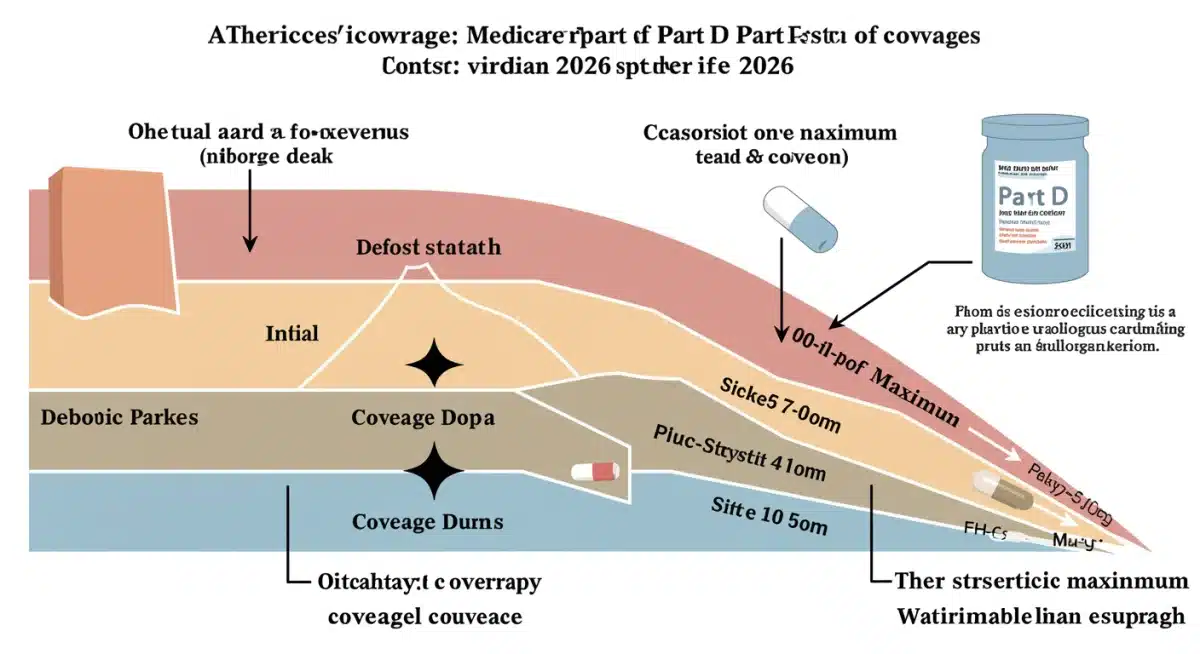

The New $2,000 Out-of-Pocket Cap: What It Means for You

The introduction of a $2,000 annual out-of-pocket maximum for Medicare Part D beneficiaries in 2026 is arguably the most significant change from the Inflation Reduction Act. This cap is designed to protect individuals from excessive prescription drug costs, offering a new level of financial security. For many, this will mean predictable spending and a substantial reduction in the financial strain associated with high-cost medications.

Currently, once beneficiaries reach the catastrophic coverage phase, they are still responsible for 5% of their drug costs, with no upper limit. This can lead to thousands of dollars in annual expenses for those on expensive treatments. The $2,000 cap effectively removes this open-ended liability, ensuring that once that threshold is met, all subsequent covered prescription drug costs for the year are paid by the plan and manufacturers.

How the $2,000 Cap Works

- Tracking Your Spending: All your spending on covered prescription drugs, including deductibles and co-payments, will count towards the $2,000 limit.

- Catastrophic Coverage Phase: Once you hit the $2,000 cap, you will immediately enter the catastrophic coverage phase, and your out-of-pocket costs for covered drugs will become zero for the rest of the year.

- Impact on High-Cost Drugs: This is particularly beneficial for individuals taking expensive specialty drugs for chronic conditions like cancer, multiple sclerosis, or rheumatoid arthritis.

This cap will provide immense relief, transforming the financial planning for many beneficiaries. It shifts the burden of ultra-high drug costs away from individuals, making essential treatments more attainable. The change also encourages better adherence to medication regimens, as the fear of exceeding a financial limit will be removed once the cap is met.

It’s important to note that the $2,000 cap applies to out-of-pocket spending on covered Part D prescription drugs only. It does not include spending on drugs not covered by your plan, or other medical expenses. Therefore, understanding your plan’s formulary and overall benefits remains crucial. The new cap is a powerful tool for cost savings, but it requires beneficiaries to continue to be proactive in managing their drug coverage. This significant change promises a future where access to life-saving medications is not dictated by an unpredictable financial burden, fostering greater peace of mind for millions.

Restructuring the Catastrophic Coverage Phase

The catastrophic coverage phase of Medicare Part D is undergoing a significant overhaul in 2026, directly linked to the new $2,000 out-of-pocket cap. Historically, this phase provided some relief, but beneficiaries were still responsible for 5% of their drug costs, a percentage that could still amount to thousands of dollars for those with very high drug expenses. The changes introduced by the Inflation Reduction Act completely eliminate this 5% coinsurance once a beneficiary reaches the catastrophic phase.

This means that after a beneficiary has spent $2,000 out of their own pocket on covered prescription drugs, they will pay nothing for any further covered medications for the remainder of the year. This is a profound shift, offering complete financial protection against extremely high drug costs. The financial responsibility for these costs will now be borne more heavily by drug manufacturers and Part D plans, rather than the individual.

Who Pays in the New Catastrophic Phase?

- Drug Manufacturers: Will contribute a higher percentage of costs for brand-name drugs in the catastrophic phase.

- Part D Plans: Will also bear a greater share of costs, particularly for generic drugs, providing an incentive to negotiate lower prices.

- Medicare: The federal government’s share will also be adjusted, reflecting the overall redistribution of costs.

This restructuring is designed to incentivize all stakeholders—manufacturers, plans, and the government—to work towards lowering drug prices and improving cost efficiency. By shifting more of the financial burden away from beneficiaries in the catastrophic phase, the system aims to provide a stronger safety net. It also addresses a long-standing criticism of Part D, which was the unlimited liability for high-cost drug users.

The elimination of the 5% coinsurance is not just about cost savings; it’s about equitable access to life-sustaining medications. No longer will individuals have to choose between crucial treatments and financial ruin due to the open-ended nature of catastrophic coverage. This change ensures that once the $2,000 threshold is met, beneficiaries can focus on their health without the added stress of looming drug bills. It represents a significant step towards a more humane and fiscally responsible prescription drug program under Medicare Part D.

Strategies for Maximizing Cost Savings in 2026

With the significant changes to Medicare Part D in 2026, beneficiaries have new opportunities to maximize their cost savings. Navigating these changes effectively requires proactive planning and a thorough understanding of your options. The new $2,000 out-of-pocket cap is a powerful tool, but maximizing its benefit involves more than just waiting to hit the limit.

One of the most effective strategies remains careful plan selection. Annual enrollment periods are critical times to review and compare Part D plans. Even with the new cap, plans will still vary in premiums, deductibles, and formularies (lists of covered drugs). Choosing a plan that best aligns with your specific medication needs can lead to substantial savings, even before reaching the $2,000 cap.

Key Strategies for Cost Savings

- Annual Plan Comparison: Always review your current plan and compare it with others during the annual enrollment period. Use Medicare’s Plan Finder tool.

- Formulary Check: Ensure your prescription drugs are covered by your chosen plan and at the lowest possible tier. Generic alternatives are often the most cost-effective.

- Pharmacy Networks: Verify that your preferred pharmacies are in your plan’s network, as out-of-network pharmacies can result in higher costs.

- Utilize Extra Help: If you have limited income and resources, apply for Medicare’s Extra Help program, which can significantly reduce premiums, deductibles, and co-payments.

Beyond plan selection, actively managing your prescriptions throughout the year can also yield savings. Discussing generic or preferred brand alternatives with your doctor, exploring patient assistance programs offered by pharmaceutical companies, and using mail-order pharmacies for maintenance medications can all contribute to keeping your costs down. Remember, the $2,000 cap is an annual limit, so spreading out your costs or finding ways to reduce them before hitting the cap still benefits your overall financial health.

Furthermore, understanding the different phases of Part D coverage—deductible, initial coverage, and the new catastrophic phase—will help you anticipate your spending. Being aware of where you are in your coverage cycle can inform decisions about when to fill prescriptions or if a change in medication might be beneficial. By combining diligent plan selection with ongoing prescription management, beneficiaries can truly maximize the cost-saving opportunities presented by the 2026 Medicare Part D changes.

Navigating Plan Options and Enrollment Periods for 2026

Navigating the various Medicare Part D plan options and understanding the enrollment periods is more critical than ever as we approach 2026. While the new $2,000 out-of-pocket cap offers significant protection, the nuances of individual plans will still play a crucial role in determining your overall prescription drug costs and access to specific medications. Choosing the right plan can mean the difference between significant savings and unnecessary expenses.

The Annual Enrollment Period (AEP), typically from October 15 to December 7 each year, is your primary opportunity to review and switch Part D plans for the upcoming year. During this time, you can compare different plans based on their premiums, deductibles, formularies, and pharmacy networks. With the 2026 changes, it’s essential to not only look at the basic costs but also how each plan integrates the new out-of-pocket cap and restructured catastrophic coverage.

Key Considerations for Plan Selection

- Formulary Review: Check if your specific medications are on the plan’s formulary and what tier they fall into. Higher tiers generally mean higher co-payments.

- Preferred Pharmacies: Confirm if your preferred pharmacy is part of the plan’s network to avoid higher out-of-network costs.

- Premium vs. Deductible: Balance a lower monthly premium with a potentially higher deductible, considering your anticipated drug usage.

- Star Ratings: Medicare assigns star ratings to plans based on quality and performance; consider these ratings during your selection process.

Beyond the AEP, certain Special Enrollment Periods (SEPs) may allow you to change plans outside of the regular window, such as if you move, lose other credible drug coverage, or qualify for Extra Help. It is vital to understand if you qualify for an SEP to ensure continuous and appropriate coverage. Remember, plan offerings can change annually, so a plan that was ideal for you last year might not be the best fit for 2026, especially with the new reforms.

Utilizing resources like the official Medicare Plan Finder tool on Medicare.gov is highly recommended. This tool allows you to input your medications and pharmacies to get personalized cost estimates for different plans. Seeking advice from a State Health Insurance Assistance Program (SHIP) counselor, who offers free, unbiased Medicare counseling, can also be invaluable. By being proactive and informed during enrollment periods, beneficiaries can confidently navigate the 2026 changes and secure the most beneficial Part D coverage for their needs.

The Broader Implications for Healthcare and Beneficiaries

The changes to Medicare Part D in 2026 extend beyond individual cost savings, carrying broader implications for the entire healthcare ecosystem and the quality of life for beneficiaries. By capping out-of-pocket spending and restructuring the catastrophic phase, the Inflation Reduction Act aims to create a more equitable and sustainable prescription drug program, fostering improved health outcomes and reducing systemic burdens.

One significant implication is the potential for improved medication adherence. When prescription drug costs are a major barrier, beneficiaries may skip doses, split pills, or forgo filling prescriptions altogether. The new $2,000 cap mitigates this financial pressure, making it more likely that individuals will take their medications as prescribed, leading to better management of chronic conditions and fewer adverse health events. This, in turn, can reduce hospitalizations and emergency room visits, ultimately lowering overall healthcare costs.

Broader Impacts of Part D Changes

- Improved Health Outcomes: Enhanced adherence to medication can lead to better management of chronic diseases and overall health.

- Reduced Healthcare System Strain: Fewer preventable hospitalizations and emergency visits due to unmanaged conditions.

- Enhanced Financial Security: Beneficiaries will experience less financial stress and can better plan for healthcare expenses.

- Market Changes: Increased pressure on drug manufacturers and Part D plans to control costs and offer competitive pricing.

Moreover, the shifting of cost responsibility to drug manufacturers and Part D plans in the catastrophic phase creates new incentives. Manufacturers might face increased pressure to justify high drug prices, potentially leading to more reasonable pricing strategies. Part D plans, now bearing a greater financial risk, will have a stronger impetus to negotiate aggressively with manufacturers and to implement effective utilization management strategies that prioritize cost-effective treatments without compromising patient care.

For beneficiaries, the peace of mind that comes with a predictable spending limit is invaluable. It allows them to focus on their health rather than worrying about overwhelming drug bills. This improved financial security can also free up resources for other essential needs, enhancing their overall quality of life. The 2026 changes represent a significant step towards a more patient-centered prescription drug benefit, one that prioritizes affordability and access, ultimately benefiting individuals and strengthening the Medicare program as a whole.

| Key Point | Brief Description |

|---|---|

| $2,000 Out-of-Pocket Cap | Limits annual spending on covered Part D drugs to $2,000 for beneficiaries, providing significant financial protection. |

| Catastrophic Phase Overhaul | Eliminates the 5% coinsurance in the catastrophic phase, meaning beneficiaries pay nothing after reaching the $2,000 cap. |

| Inflation Reduction Act (IRA) | The legislation responsible for these major Part D reforms, aiming to reduce drug costs and improve affordability for beneficiaries. |

| Proactive Plan Selection | Crucial for maximizing savings; compare plans during AEP to match formulary, premiums, and deductibles to individual needs. |

Frequently Asked Questions About Medicare Part D in 2026

The most significant change is the introduction of a $2,000 annual out-of-pocket spending cap for covered prescription drugs. This means beneficiaries will not pay more than $2,000 out of their own pocket for Part D medications in a calendar year, providing substantial financial protection.

In 2026, the 5% coinsurance that beneficiaries currently pay in the catastrophic coverage phase will be eliminated. Once you reach the $2,000 out-of-pocket cap, you will pay nothing for covered prescription drugs for the remainder of the year, enhancing financial relief.

After a beneficiary reaches the $2,000 cap, the financial responsibility for covered drug costs shifts primarily to drug manufacturers and Medicare Part D plans. This redistribution of costs aims to reduce the burden on individuals and incentivize cost management.

To best prepare, carefully review your current Part D plan during the Annual Enrollment Period (October 15-December 7). Compare available plans, check their formularies for your medications, and consider how the new $2,000 cap will impact your potential out-of-pocket spending for 2026.

While the new cap limits out-of-pocket drug costs, monthly premiums for Part D plans can still vary and may change annually. It’s crucial to compare premiums alongside deductibles and drug coverage when selecting a plan to ensure it meets your budget and medication needs.

Conclusion

The year 2026 marks a transformative period for Medicare Part D beneficiaries, ushering in changes that promise greater financial predictability and relief from high prescription drug costs. The implementation of a $2,000 annual out-of-pocket cap and the restructuring of the catastrophic coverage phase are monumental steps towards making essential medications more affordable and accessible. These reforms, stemming from the Inflation Reduction Act, underscore a commitment to protecting seniors and individuals with disabilities from the escalating burden of drug expenses.

Understanding these upcoming changes is not merely about compliance; it’s about empowerment. By proactively engaging with information about the new benefits, carefully reviewing plan options during enrollment periods, and strategically managing prescription drug use, beneficiaries can optimize their coverage and significantly reduce their healthcare expenditures. The landscape of prescription drug benefits is evolving, and staying informed is the best defense against potential financial surprises. Ultimately, these changes are designed to foster better health outcomes and provide much-needed peace of mind for millions of Americans relying on Medicare Part D.